Welcome to the first post in our six-part series on cryptocurrency accounting under IFRS. This topic might seem far removed from drill programs and assay results. However, it’s increasingly relevant to Canadian mineral exploration companies.

Whether your company has dipped its toes into crypto or you’re simply curious, this series will give you clarity. Here’s the thing: even at the beginning of 2026, there’s still no dedicated IFRS standard for crypto assets. Consequently, companies are piecing together guidance from IAS 38, IAS 2, and IFRS 13. Many get cryptocurrency accounting wrong.

Cryptocurrency Accounting Challenges for Mining Companies

Bitcoin launched in 2009. Most of us in the mining sector dismissed it as internet funny money.

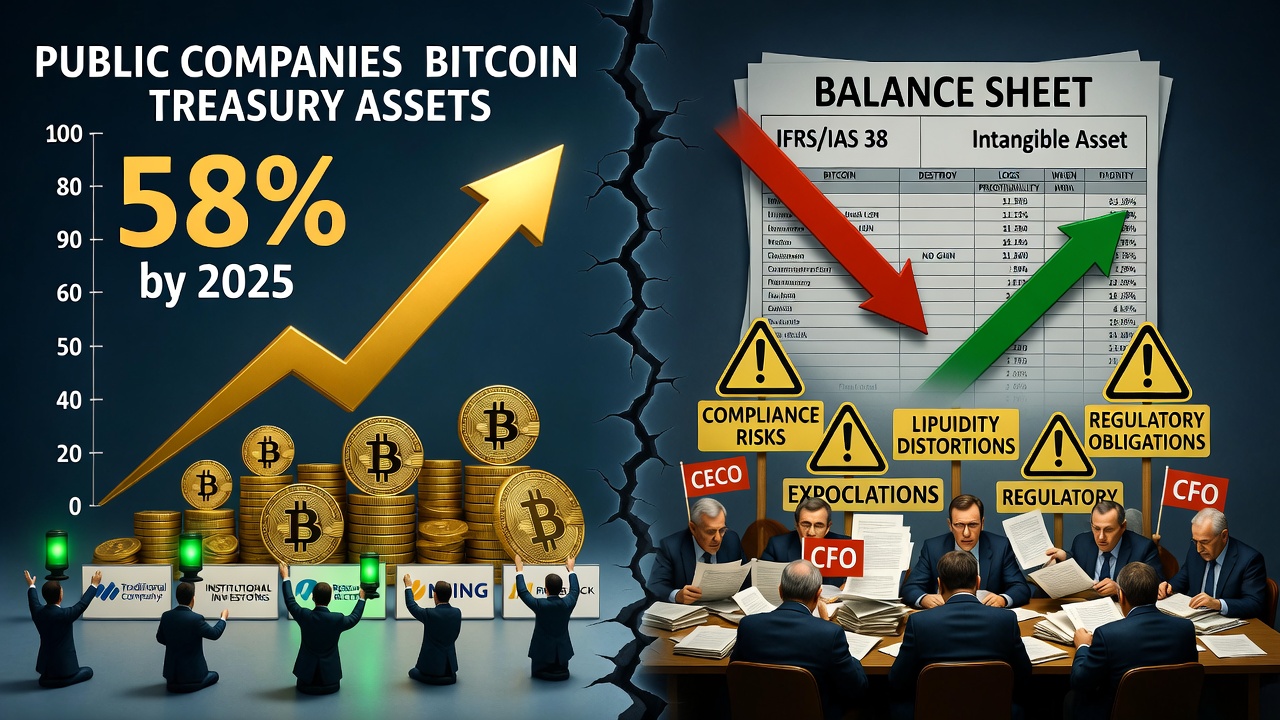

Today, things look different. We’re looking at over 10,000 different cryptocurrencies. In 2025, publicly listed companies holding Bitcoin increased by 58%. These are real companies with real regulatory obligations.

So why should you care? There are three key reasons.

Business Adoption of Cryptocurrency Payments

First, business adoption is accelerating. Some mining equipment suppliers now accept Bitcoin. For instance, if a vendor offers a 2% discount for crypto payment, you need to understand the implications first. That seemingly simple transaction creates a cascade of financial reporting challenges.

Cryptocurrency Accounting for Treasury Strategy

Second, some junior exploration companies hold Bitcoin as part of their working capital strategy. They may allocate 5-10% for potential appreciation.

However, the cryptocurrency accounting treatment will significantly impact your financial statements. It affects liquidity ratios. Moreover, it can impact your ability to satisfy TSX-V continued listing requirements.

The Volatility Problem in Cryptocurrency Accounting

Third, Bitcoin can swing 30% in a week. Your fractional CFO delivers statements showing crypto holdings at $500,000.

Three days later at your board meeting? Those holdings might be worth $350,000. Or $650,000.

How do you make strategic decisions with that instability?

Current IFRS Guidance on Cryptocurrency Accounting

Here’s where it gets technical. Under current IFRS guidance, cryptocurrencies are NOT classified as cash or cash equivalents. The June 2019 IFRS Interpretations Committee decision is still authoritative in 2026. We’ll discuss this in detail in part 2.

For most companies, crypto gets classified as intangible assets under IAS 38. These assets are subject to impairment testing. But they don’t get marked to market for increases. We’ll get into all of that in part 4.

Think about the practical impact.

Say your Bitcoin holdings drop from $500,000 to $350,000. You must recognize a $150,000 impairment loss. This crushes your profitability metrics.

But what if holdings rise to $650,000? Under IAS 38’s cost model, you recognize nothing until you sell. As a result, your balance sheet is understated. Consequently, investors get a distorted picture of your financial position.

TSX-V Listing Requirements and Cryptocurrency Accounting

This becomes particularly problematic for TSX-V listing requirements.

For example, say you’ve got $2 million in crypto classified as an intangible asset. It might not count toward your working capital calculation. Suddenly, you’re scrambling to explain your liquidity position to regulators.

Accepting crypto payments from investors adds another layer. First, you need to determine fair value at transaction date. Next, you must classify it appropriately. Additionally, you need custody controls. Finally, you must track subsequent measurement requirements.

If your fractional CFO is already delivering bare-minimum statements at the last minute? This is asking for disaster.

Why You Need Specialized Cryptocurrency Accounting Expertise

The bottom line: cryptocurrency accounting requires deep technical expertise. Specifically, you need knowledge of both IFRS standards and digital assets.

Ideally, you need someone who can proactively guide you through classification decisions. They must understand measurement approaches and disclosure requirements.

The stakes are too high. The regulations are too complex. Therefore, you can’t navigate this alone.

Conclusion

We’ve established why cryptocurrency accounting matters for mineral exploration companies. The fundamental challenge: IFRS wasn’t designed for digital assets. Yet companies must make do with existing standards.

The result? Inconsistent classification. Distorted financial metrics. Real compliance risks.

In our next post, we’ll dive deeper. Specifically, we’ll explore why cryptocurrencies don’t qualify as cash or financial instruments. This determination has massive implications for your balance sheet and liquidity reporting.

And if you’re thinking, “My fractional CFO definitely isn’t equipped to handle this,” you’re probably right. Perhaps it’s time to explore what specialized, exploration-focused financial leadership actually looks like.